Tax preparation workflows in most CPA firms follow predictable, yet painfully manual, patterns:

- Receive the raw client trial balance.

- Prepare data for entry by cleaning it up in Excel.

- Analyze accounts to identify misclassifications and calculate adjustments.

- Mannually key every account balance and figure into the tax software.

- Complete the tax forms, elections, and diagnostics.

- Review the final return for accuracy and professional compliance.

Each step involves error-prone, manual data handling, critical decision-making, and labor-intensive quality checks. Some steps are significant bottlenecks where work piles up for hours. Others are hidden sources of error (such as transposed digits) that cause massive amounts of rework later. The cumulative effect is that your firm's tax season capacity is strictly limited by the speed and accuracy of these slow, manual input processes.

Workflow automation addresses these painful constraints not by magically "importing" data, but by eliminating the need for manual data entry entirely. By standardizing processes and catching errors digitally before you ever touch a keyboard, automation transforms how you work. For CPA firms preparing business returns, this translates directly to higher capacity with the same staff, shorter turnaround times, and fewer frustrating errors requiring correction at the eleventh hour.

The Standard Tax Prep Workflow (And Where Time Goes)

Understanding where time is spent reveals where automation delivers the most value.

Step 1: Trial Balance Receipt and Initial Review (10 to 20 Minutes)

Client sends trial balance. Staff opens the file, checks the format, and assesses whether it’s usable. If the format is problematic, staff requests a different export or begins manual reformatting.

Time sink: The back-and-forth with clients requesting different file formats, waiting for responses, and restarting the workflow when new files arrive.

Step 2: Trial Balance Preparation (45 to 90 Minutes)

Once the raw data is exported, staff must transform "client-ready" reports into "tax-ready" data. This involves intensive manual data wrangling: stripping out subtotals, standardizing column headers, fixing broken number formats, and reconciling current-year figures against prior-year ending balances.

Template Trap: While many firms use Excel templates to streamline this process, the bottleneck remains significant.

Time sink: Staff members lose hours to repetitive "cleanup" tasks that vary slightly by client’s accounting system (e.g., QuickBooks Online vs. Xero) but follow the same tedious patterns.

The Cost: This stage often consumes senior-level time on administrative data entry rather than high-level tax strategy or technical review, delaying the entire engagement lifecycle.

Step 3: Account Classification and Cleanup (30 to 60 Minutes)

This step moves from data entry to professional judgment. The preparer conducts a meticulous, line-by-line review of the client's trial balance.

The goal is to perform account normalization: identify compliance risks, detect material misclassifications, determine necessary adjusting journal entries (AJEs), calculate the exact adjustment amounts, and apply those changes to the working trial balance.

Time sink: Line-by-line account review, mental context switching between client books and tax requirements, calculation of adjustments.

Step 4: Tax Software Data Input(30 to 60 Minutes)

In this stage, the "clean" data from your spreadsheet must be moved into the tax software. Because many systems lack a direct link, the standard reality for many firms is manual data entry. This requires the preparer to meticulously key in every account balance, hand-calculate subtotals where necessary, and validate that the final digital trial balance matches the workpaper precisely.

Time sink: This is a high-stakes "stare-and-compare" exercise. The preparer must switch between a spreadsheet and the tax software, manually entering figures while ensuring they land in the correct tax fields. This repetitive re-keying is not just slow; it is the primary source of transcription errors (like transposed digits) in the return.

The Validation Loop: Once the data is entered, the preparer must perform a line-by-line reconciliation to ensure the software’s total matches the spreadsheet. If the numbers don't tie, the preparer must audit their own data entry to find the typo.

Step 5: Tax Form Completion & Diagnostics (45 to 90 Minutes)

This stage converts the raw numbers into a compliant tax return. The preparer completes all necessary forms, makes critical tax elections, calculates complex, tax-specific items (e.g., depreciation differences), and adds all required supporting schedules. The final step involves running the tax software's internal diagnostics and fixing any errors or warnings it flags.

Time sink: The main time sink here isn't the tax work itself, but rather the "garbage-in, garbage-out" effect of earlier manual steps. When the initial trial balance entry in Step 4 contains errors or misclassifications, those issues surface here as diagnostic failures. The preparer must repeatedly stop their flow, backtrack through the workpapers to diagnose the original typo or omission, fix the trial balance data, and then re-run diagnostics.

Step 6: Review & Finalize (30 to 90 Minutes)

This crucial final step is the quality control checkpoint. The reviewer conducts a meticulous assessment of the entire return for accuracy, reasonableness, compliance with current tax law, proper classifications, and the presence of any required items. If issues are found, from simple transcription errors to material classification problems, the return is sent back to the preparer for correction.

The Time Sink (The Rework Loop): This stage is where firm capacity often buckles under pressure. The biggest time sink is the "rework loop" caused by issues found during the review. The back-and-forth communication needed to understand a preparer’s manual entry choices or simply identify a transposed digit from Step 4 consumes valuable senior-level time. Every error found here forces a full loop back through the process, delaying final filing and consuming resources that should be dedicated to other client engagements.

Total Time Per Return

For a moderately complex business return, you're looking at three to seven hours of staff time from trial balance receipt to filing. Simple returns might take two hours. Complex returns can take ten or more hours. A significant chunk of that time (often the majority) is spent on data preparation and cleanup rather than on tax expertise.

What Workflow Automation Actually Does

Automation doesn't touch every step equally. It focuses on the bottlenecks and error sources that consume disproportionate time or create rework. Here’s what changes:

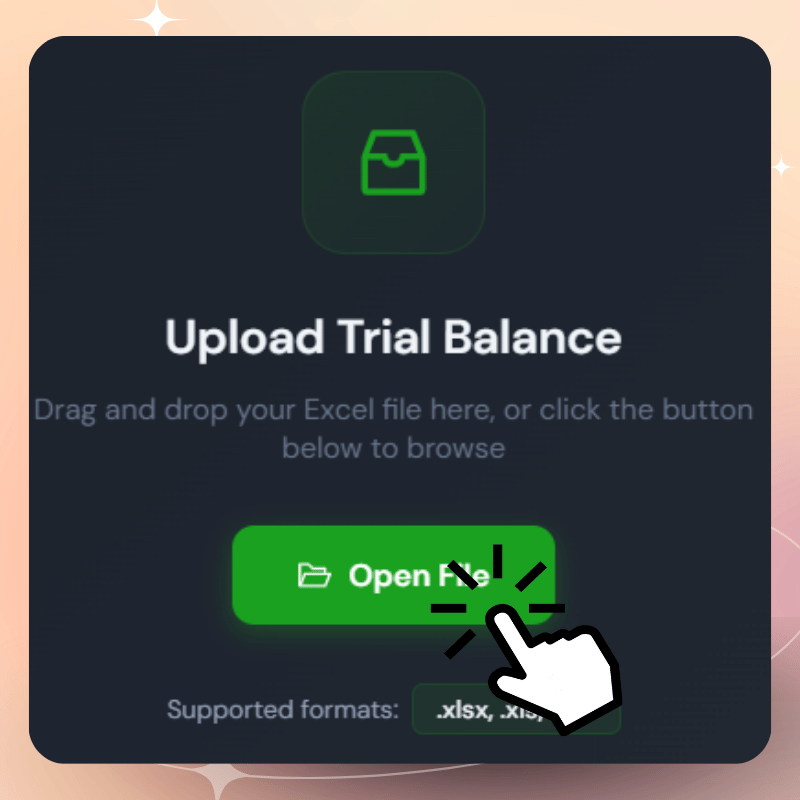

Direct Import or Upload

The workflow starts with getting the trial balance into the system. Users can either connect directly to QuickBooks to pull the trial balance automatically or upload a trial balance file from any accounting system. No more requesting specific file formats from clients or reformatting files to match your template. The software accepts the data as it comes.

Automatic Column Detection and Standardization

Once the trial balance is imported or uploaded, the software automatically detects columns regardless of how the source system labeled them. Account names, debits, credits, beginning balances, and ending balances get identified and organized into a standardized format. Subtotals and section headers are removed. The trial balance is validated to ensure it balances.

The result is a clean, standardized trial balance ready for adjusting entries. This happens in seconds, not the 45 to 90 minutes staff currently spend on manual reformatting.

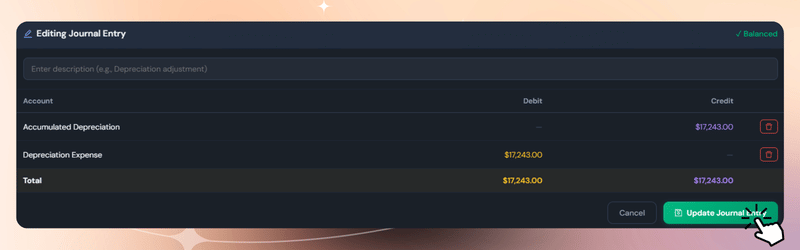

Adjusting Journal Entries

With the trial balance in a standardized format, preparers can make adjusting entries directly in the software. Common adjustments for depreciation, meals and entertainment limitations, loan principal, and other tax-specific items can be entered and applied. The software tracks all adjustments with a full audit trail. Prior year adjustments can be referenced and reapplied where appropriate.

What used to require copying and pasting between Excel templates and manual calculations becomes a streamlined process within a single interface.

Account Classification and Tax Mapping

Once adjustments are complete, the adjusted balances must be mapped to the firm’s specific tax software. The software knows how accounts should be classified for each client and remembers those mappings year over year. For returning clients, accounts are automatically mapped based on the prior year’s configuration. Only new accounts require mapping decisions. The preparer reviews the mapping, makes any needed changes, and confirms the classification is correct for the current year.

Export for Tax Software

The final step is creating a file that the tax software can import directly. The software exports the adjusted, properly classified trial balance in the exact format required by your tax software. This file can be uploaded to auto-complete much of the return, eliminating manual data entry for account balances and reducing the risk of transcription errors. The preparer opens the tax software to a return that's already populated with clean, adjusted data ready for tax-specific work.

The Math That Matters: Per-Return Time Reduction

In a manual workflow, pre-tax-prep time typically breaks down like this: 45 to 90 minutes on trial balance prep and reformatting, 30 to 60 minutes on making adjusting entries and calculating adjustments, 30 and 60 minutes on tax software manual data entry, and 15 to 45 minutes on rework from late-discovered errors. Total pre-tax-prep time runs 120 to 255 minutes. That's 2 to 4.25 hours before a reviewer even looks at the return.

With automation, the same work compresses dramatically. Trial balance import and standardization happen automatically in under a minute. Making adjusting entries takes 10 to 20 minutes in a clean interface with prior year reference. Account mapping takes 2 to 5 minutes for returning clients since mappings are remembered. Exporting and importing to tax software takes 2 to 3 minutes. Total pre-tax-prep time: 15 to 30 minutes.

By replacing manual entry with a digital workflow, you can save up to 3.75 hours per business return. This time savings has broader implications at the firm level. The time and cost saved can be redirected, allowing your staff to concentrate on technical tax strategy rather than data entry.

Capacity Impact Across Tax Season

Time savings per return compound across a full client base. Consider three scenarios.

50 Business Returns: Manual workflow consumes 163 hours of pre-tax-prep work. Automated workflow requires 27 hours. Time saved: 136 hours, which is 3.4 weeks of full-time work.

150 Business Returns: Manual workflow: 488 hours. Automated workflow: 80 hours. Time saved: 408 hours, or 10 weeks of full-time work.

300 Business Returns: Manual workflow: 975 hours. Automated workflow: 160 hours. Time saved: 815 hours, which equals 20 weeks of full-time work.

Twenty weeks of full-time work freed up across tax season changes what's possible for your firm. You can prepare more returns with existing staff, reduce overtime hours during tax season, improve review quality by allocating more time to complex returns, accept new clients without adding headcount, or reduce tax season extension rates by completing more returns by deadline.

Capacity for Regulatory Compliance and Advisory Services

The benefits of workflow automation extend far beyond processing more tax returns. For CPA firms, time savings create something even more valuable: capacity. As regulatory requirements continue to expand, firms need more time to stay informed, advise clients, and help businesses navigate increasingly complex compliance obligations.

Today, business owners expect more than tax preparation. They look to their CPA as a trusted advisor who can help them understand what filings, licenses, registrations, and ongoing requirements apply to their business. Questions often go beyond tax itself: What reports need to be filed? Are there local licensing requirements? Are there state-specific obligations or industry regulations to monitor? Clients increasingly expect their CPA to either have the answers or guide them toward the right resources.

Recent developments illustrate how quickly compliance requirements can emerge and change. The rollout and subsequent legal reversal of Beneficial Ownership Information Reporting (BOIR) requirements demonstrated how rapidly businesses can face new obligations, and how quickly those obligations can evolve. Firms that stayed informed were better positioned to guide clients through uncertainty.

And BOIR was only one example. State licensing rules continue to change. Sales tax nexus standards evolve as states refine economic presence rules. Data privacy laws expand. Corporate transparency initiatives introduce new reporting obligations. Industry-specific regulations continue to grow across healthcare, financial services, professional services, and other sectors.

Running an efficient practice isn't simply about speeding up workflows or reducing administrative tasks. It's about creating the capacity to understand regulatory nuance, stay ahead of changes, and provide the guidance clients increasingly depend on. The firms that embrace automation gain more than efficiency: they gain the ability to better protect and advise their clients.

Beyond Time Savings: Process Standardization

Workflow automation also standardizes how work is done, which has benefits beyond pure time savings.

Consistency Across Preparers

Manual processes vary by who's doing the work. One preparer might catch misclassifications that another misses. One person's cleanup standards might be more thorough than another's. Automation applies the same rules, checks, and classifications regardless of who initiates the workflow. This produces consistent quality across your entire return volume, which matters for both client service and risk management.

Workflow automation also standardizes how work is done, which has benefits beyond pure time savings.

Reduced Training Burden for New Staff

Training new preparers on trial balance cleanup takes time. They need to learn what to look for, how to identify problems, what adjustments to make, and how your firm does things.

When cleanup is automated, new staff review flagged issues and suggested corrections rather than learning to identify problems from scratch. This shortens the learning curve and allows junior staff to contribute earlier.

Institutional Knowledge Capture

Experienced preparers know client-specific quirks: this client always has meals in travel, that client needs vehicle expense split 60/40, another client requires specific depreciation handling.

This knowledge typically lives in preparers' heads. When that person is out or leaves the firm, the knowledge goes with them.

Automation captures these decisions as client-specific rules that persist year over year regardless of staff changes.

Easier Reviewer Oversight

Reviewers currently need to check that trial balance prep was done correctly: were misclassifications caught, were adjustments calculated properly, did the import work cleanly?

With automation, these steps follow standard processes with audit trails. Reviewers can focus on tax positions and complex areas rather than verifying data preparation quality.

Common Concerns About Workflow Automation

Will Automation Replace Preparer Judgment?

No. Automation handles pattern recognition and rule application. Preparers still make decisions about unusual situations, tax positions, elections, and client-specific circumstances.

The difference is that preparer time shifts from repetitive data handling to higher-value judgment calls.

What If Automation Makes a Mistake?

Automation suggests corrections rather than applying them blindly. Preparers review and approve suggestions before they're applied. If a suggestion is wrong, the preparer rejects or modifies it.

Over time, the preparer's decisions train the system to be more accurate for that client.

Does This Work for Complex or Unusual Clients?

Automation works best for common patterns. For clients with unusual accounting structures or one-off situations, automation flags what it can and leaves the rest for manual handling.

Even for complex clients, automation typically handles 60% to 80% of preparation tasks, leaving preparers to focus on the genuinely complex portions.

Will This Disrupt Our Existing Workflow?

Workflow automation integrates into the existing trial balance-to-tax software flow. Trial balances come in, automation processes them, and clean trial balances go to tax software.

The tax preparation step itself doesn't change. The automation happens before tax prep begins, so it doesn't alter how preparers use tax software.

What to Look for in Workflow Automation Software

Not all workflow automation solutions are created equal. Here's what actually matters.

Handles Multiple Accounting System Formats: Your clients use different accounting systems. Workflow automation should accept trial balances from QuickBooks, Xero, Sage, Excel, CSV, and other common sources without requiring format standardization.

Learns from Preparer Decisions: The software should remember how you handled issues for each client and apply the same logic in future years. This is what turns first-year time investment into ongoing time savings.

Integrates with Your Tax Software: Automation should export clean trial balances in the format your tax software requires. If you still need manual reformatting after automation, the integration is incomplete.

Provides Audit Trail and Documentation: Every adjustment, reclassification, and correction should be documented automatically. This supports review and provides workpaper documentation.

Allows Firm-Wide Rule Configuration: Beyond client-specific rules, you should be able to set firm-wide standards that apply to all clients. This ensures consistent treatment of common issues across your practice.

Calculating ROI for Your Firm

Whether workflow automation makes sense depends on your client volume and preparer time costs.

Time Savings Calculation

Whether workflow automation makes sense depends on your client volume and the time costs of preparers. The math is straightforward.

Start with time savings. Estimate average time saved per return, which typically runs one to 2.5 hours for business returns. Multiply by the annual business return volume. Convert to a dollar value using the preparer’s hourly rate, including salary and overhead.

Here's an example for a firm with 100 business returns. If you save 1.5 hours per return, that's 150 hours total. At a loaded cost of $60 per hour for preparer time, the annual value is $9,000. That's direct cost savings, but it's not the whole picture.

The capacity value often exceeds direct cost savings. Consider how many additional returns you could complete with the time you save. What's the revenue per additional business return? How much overtime expense could you avoid? For many firms, the ability to take on 20 or 30 additional clients without adding staff is worth more than the labor cost savings on existing clients.

Making the Change

Tax prep workflows evolved over decades to fit manual processes and legacy software constraints. Automation is now mature enough to handle the pattern recognition and rule application that consumes the majority of pre-tax-prep time. The question isn't whether automation can improve efficiency. It demonstrably can. The question is whether the time investment to implement it and train staff delivers returns that justify the cost for your specific practice.

For firms handling significant business return volume, the math usually works. The time savings compound across every return, every preparer, every tax season. Process standardization reduces quality variance and training burden. Institutional knowledge gets captured instead of walking out the door with departing staff. And preparer capacity shifts from data manipulation to tax expertise, which is what you hired them to do in the first place.

Related Resources

For specific guidance on workflow automation and efficiency:

How CPA Firms Automate Trial Balance to Tax Return Workflow

Reducing Tax Prep Bottlenecks with Trial Balance Automation

How to Standardize Tax Prep Processes Across Multiple Preparers

Trial Balance Automation ROI Calculator for CPA Firms

Streamline Your Tax Prep Workflow

If your tax prep workflow is constrained by trial balance preparation time, Ledger IQ automates the bottlenecks. The software handles trial balance import, normalization, classification, and cleanup automatically, reducing pre-tax-prep time from hours to minutes per client. This frees up preparer capacity for actual tax work and allows you to handle higher client volume with existing staff.